For this month’s edition, I thought we should look at the health of the U.S. consumer. There are two reasons for this. First, the U.S. economy is primarily driven by consumption – personal spending on goods and services. The second consideration is that typically if the U.S. is sick the rest of the world catches a cold.

Relative to the rest of the world, the U.S. equity market has underperformed to start 2025. In Matco’s 2025 annual outlook we discussed the relatively high valuations of U.S. equities, and the potential drag on market performance that follows higher valuations as earnings take time to catch up to market expectations.

About 77% of U.S. large capitalization companies have reported for the most recent quarter, showing a handsome 17.8% year-over-year earnings growth rate according to FactSet.¹ Far above that of the long run 7% average.

The high valuation of U.S. stocks requires this strong earnings growth to continue for at least another year, if not two or three to appropriately justify the current multiple. Can earnings in the U.S. continue their impressive path of growth?

By asking that question, we are really asking if personal consumption can continue its current path. As a share of nominal GDP, consumption makes up 68% of U.S. GDP.

Understanding the state of the U.S. consumer requires us to look at the situation from multiple lenses.

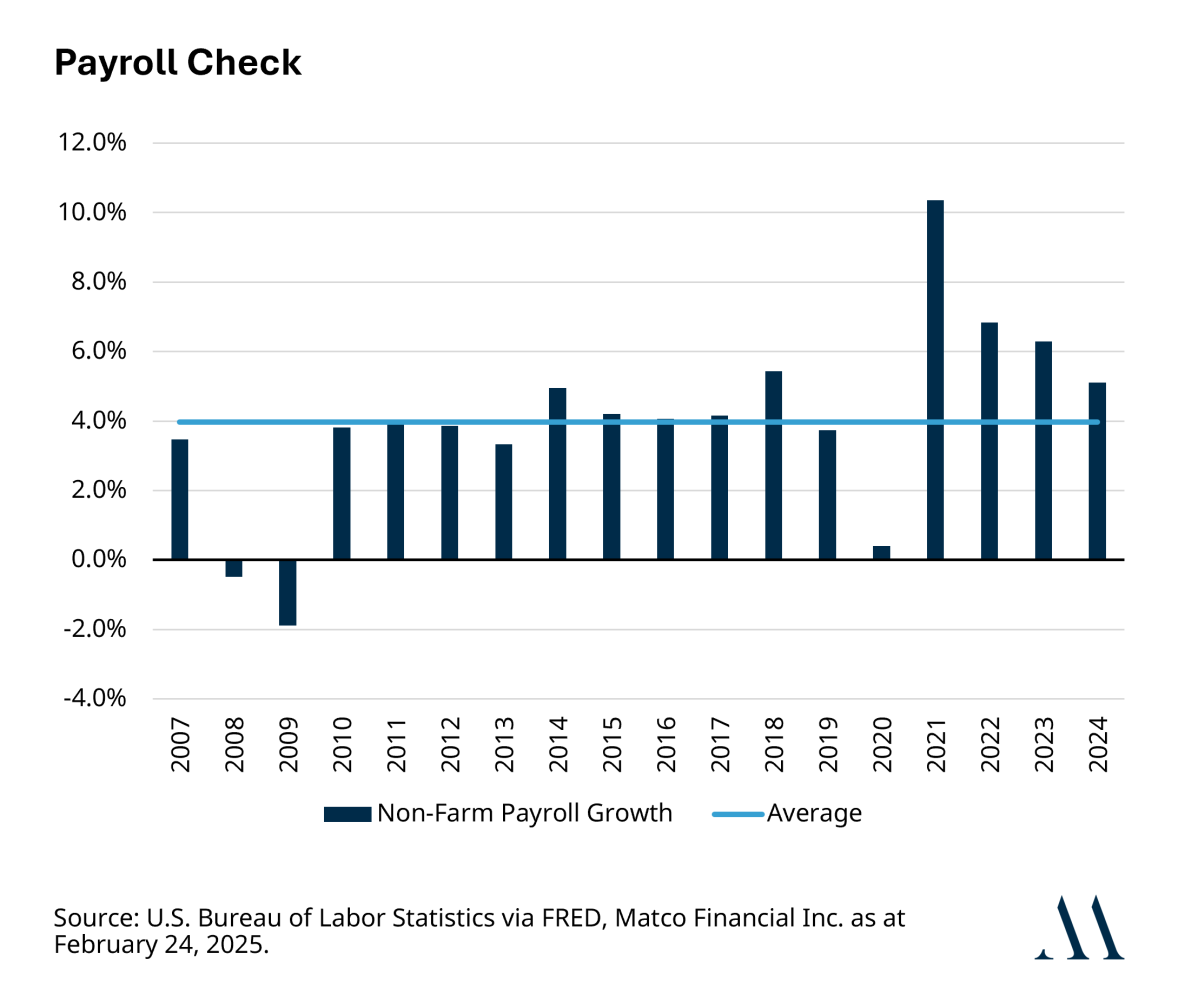

From an income perspective the average worker had a good year, average private non-farm payroll growth was a healthy 5.1% in 2024. Remember, if you are 6 feet tall and can’t swim, you can still find yourself in trouble crossing a river that is on average 5 feet deep. Nonetheless, 5.1% growth is well above the long-run average of 4% and encouraging.

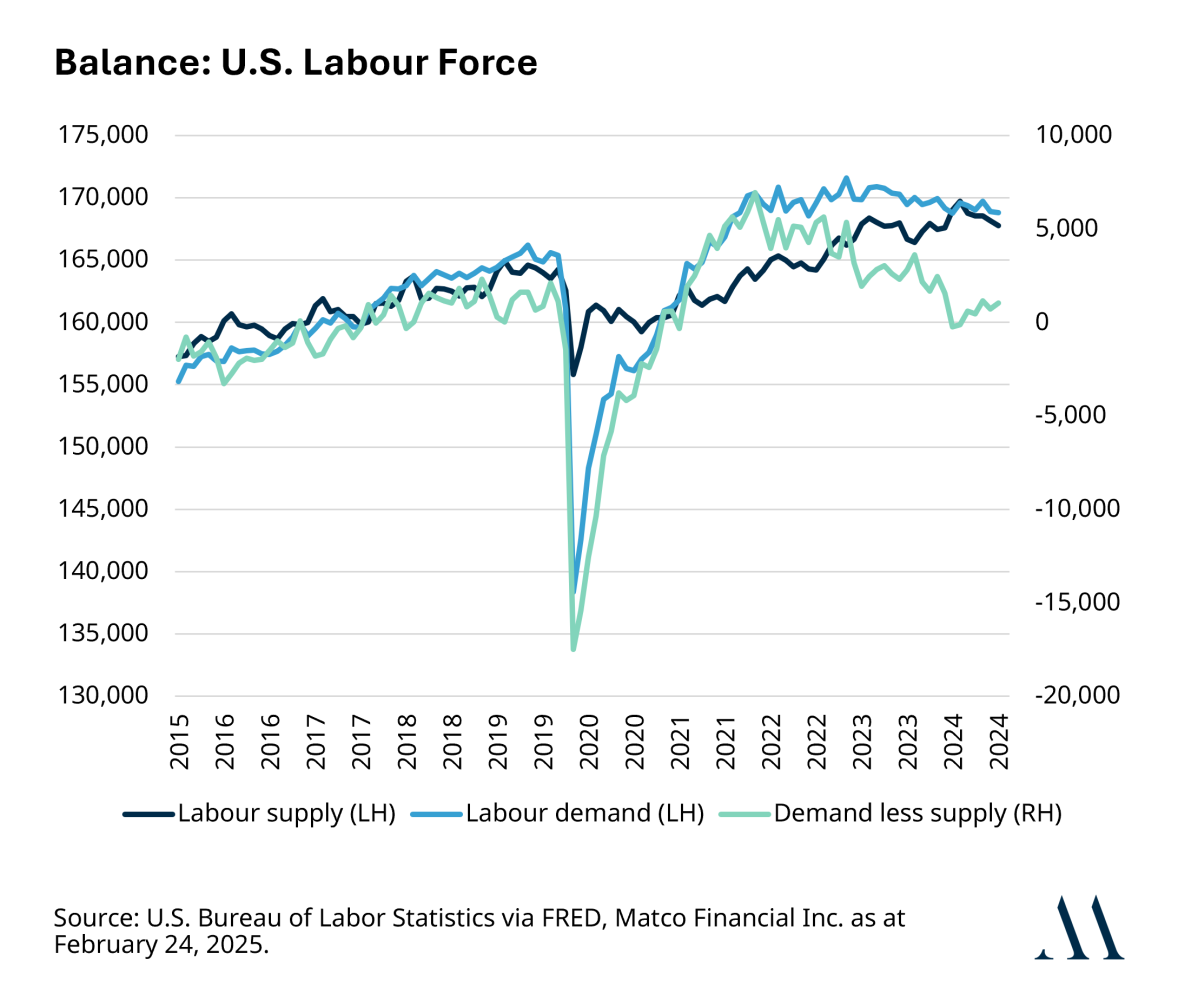

The labour market is similarly strong today. The demand for workers in the U.S. still outpaces the supply. The initial jobless claims and continuing claims remain in check. There is about one job vacancy for each unemployed person in America.

All of this is summarized by an unemployment rate that sits at 4.4% on an un-seasonally adjusted basis. Unemployment in this range a decade ago would be considered nearly full employment and largely positive – we have become accustomed to a low unemployment level that perhaps we have now forgotten how good this level really is.

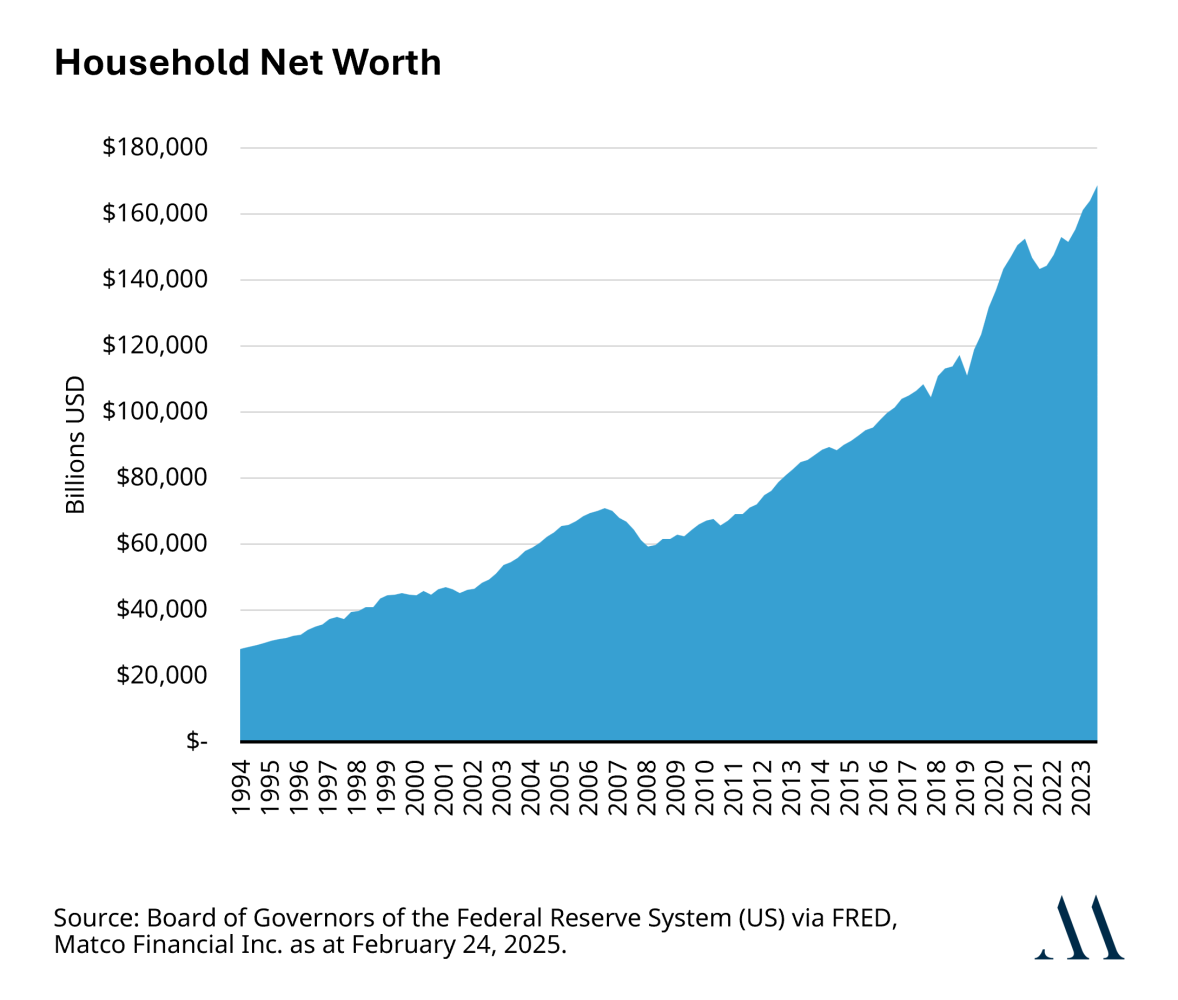

But the debt. Americans on average are worth more today than at any other time in history. Concentrated, yes. Forbes reported that in 2024 America had over 800 billionaires and that their combined net worth was 5.7 trillion. Well fast forward another year and let’s say they grew by 25%, they are worth 7.13 trillion today. According to the Federal Reserve, Household and Nonprofit Organizations Net worth is a little over 168 trillion.² Total assets are 9x the outstanding liabilities.

“You are cherry picking – the debts held by those who don’t have assets.” There is an argument here; however, mortgage debt makes up 66% of household loans.³ Meaning a good chunk of debt is backed by real assets.

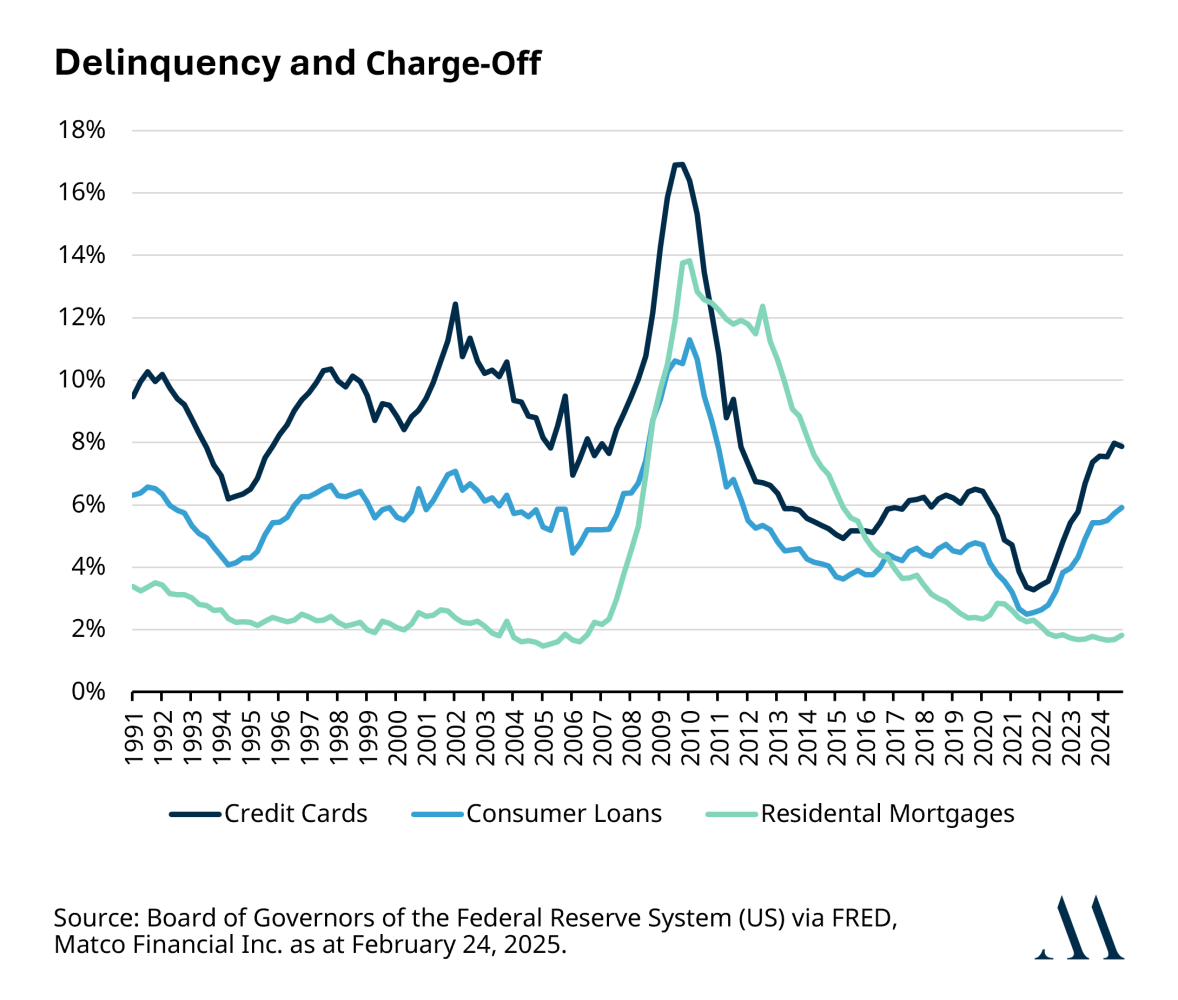

Finally, the delinquency and charge-off rates on the different forms of debt are largely in check. Delinquencies measure loan payments that are 30 days or more past due. Charge-offs refer to the loans that the banks have moved from “performing,” meaning accruing interest and being paid to those which the banks deem as “non-performing,” which means the bank has written off the loan and no longer accrues interest nor do they expect to be paid back. Yes, the credit card and consumer loan delinquency and charge-off rates have risen in the last year, but we are starting to see some stabilization in the rate of increase. On a historical basis, we are still well below the financial crisis of 2008 and largely in line with the mid-2000’s.

Despite the relatively healthy U.S. consumer, there has been some concern around the consumer confidence level. According to the University of Michigan consumer confidence survey, the level is 71.7, well below the ten-year median of 89.⁴ This decline in the consumer confidence level can largely be attributed to the increase in inflation expectations over the same period.

What are investors to do with this information? Be prepared to buy the dip. The value of investing in a well-diversified investment portfolio cannot be underestimated in this market environment. Staying invested around your target asset allocation weights appears to be justified by the fundamentals we are experiencing today. The value of diversification comes from the preservation of assets and market volatility presents opportunity. Continuing to monitor these fundamentals should help develop confidence in the future. Prudent investors follow a disciplined rebalancing process allowing them to buy weakness as they stay focused on the long term.

1.FactSet financial data and analytics

2.https://fred.stlouisfed.org/release/tables?rid=52&eid=810090#snid=810130

3.https://fred.stlouisfed.org/release/tables?rid=52&eid=810090#snid=810130