This month’s market update is a little late — I’ve been taking orders from my new boss, she is eight weeks old and not very interested in publication schedules. Between analyzing companies and perfecting the art of the diaper change, I’ve learned to embrace multi-asset balancing.

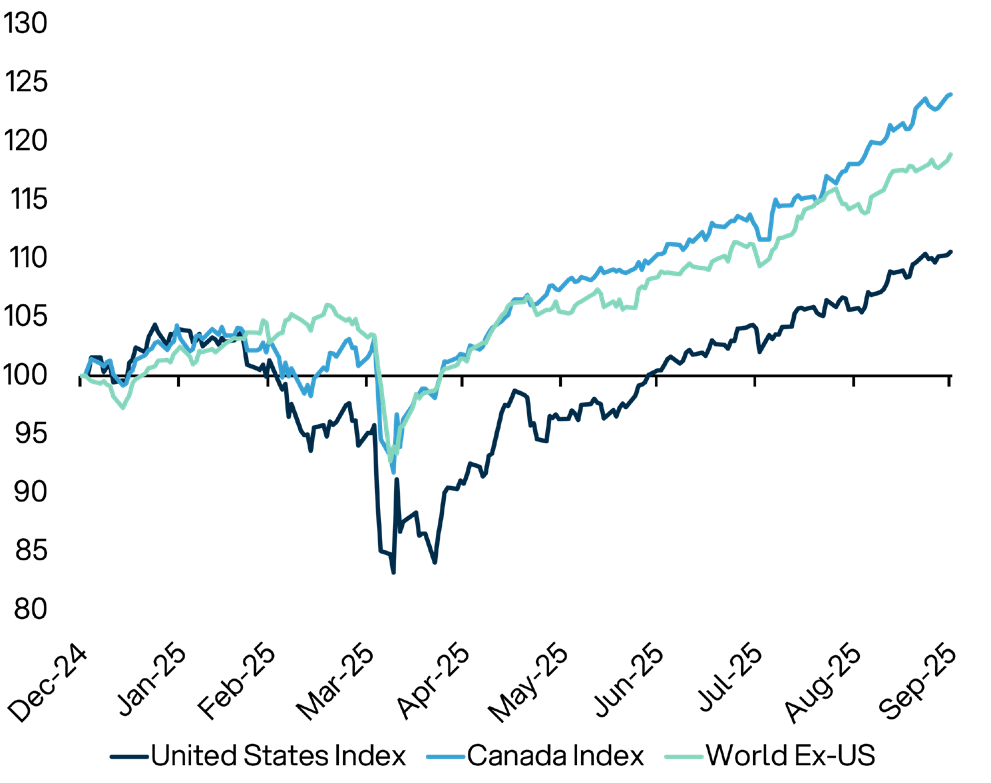

World Markets 2025

Source: FactSet Data & Analytics, Matco Financial Inc. as at September 30, 2025

In the last publication, we recapped the second quarter 2025 financial reporting period. The highlight? Better than expected. A green light to growth. Since publishing at the start of September, the U.S. central bank cut its target rate for the first time in 2025 sparking speculation of what this rate cut means for the jobs market and inflation.

Central bank rates are like the tide, raise or lower all boats as the tide comes in or goes out. The US Fed target rate is still World Markets 2025 not accommodative, but the easing of financial conditions is at least for the near term, a positive catalyst.

We are now in the third quarter reporting period with the belly of the reports arriving mid-October to mid-November. I’ll be sure to recap the quarter once most reports have been released.

For equity investors, this break in financial reporting offers a time to review the expectations for the next year, namely the balance between risk and reward. Here at Matco, this is an opportunity to review the earnings expectations for the next year, the risks to those expectations, and updating our investment framework. While the 2026 estimates have been revised modestly, the expectation is for 14-15% growth in the FactSet World Index from the 2025 numbers. About double the longer-term average of 7%.

The balance to these strong earnings estimates is higher valuations as we enter 2026. Unlike 2024 going into 2025, world ex-U.S. isn’t particularly cheap. With strong expectations for the future, valuations have expanded more quickly than the earnings themselves. The outlier is North America where earnings in 2025 have outpaced multiple expansion.

A market dynamic like this suggests that security selection rather than regional allocation will be a key differentiator in the coming year. That’s why we choose to invest in wide moat businesses, growing cash flows, and management teams with strong execution track records. By building our portfolio with these blocks we strike a balance between value and growth for long-term wealth accumulation.