Oil pulled the fire alarm in March.

Prices moved higher on rising tensions around Iran and the Strait of Hormuz. A narrow passage that carries roughly 20% of the world’s oil supply. When that route gets disrupted, prices react fast. But inflation doesn’t. It follows later, sometimes by months. And that delay is where the real opportunity begins.

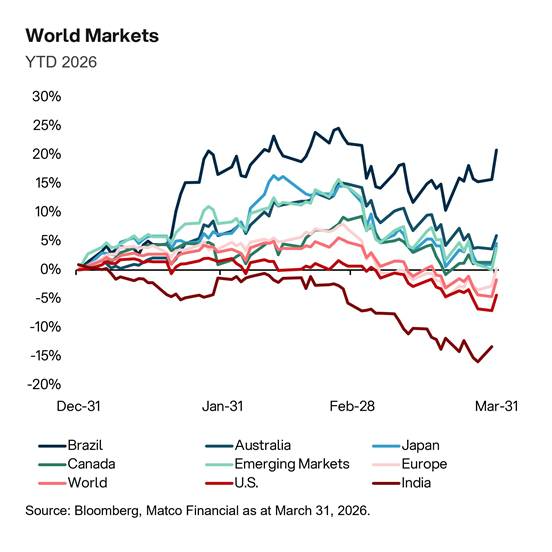

World Markets Context

The chart tells a clear story this quarter. Commodity-linked markets have led the way. Brazil is up roughly 10% year-to-date, with Australia and Canada also in positive territory. Meanwhile, the U.S. has pulled back around 4%, and India has been the weakest major market, down approximately 13% through the end of March.

The pattern makes sense. When energy prices rise, countries and sectors tied to commodity production tend to benefit. Growth-heavy markets, where valuations are more sensitive to inflation expectations, feel the pressure first. In last quarter’s newsletter on earnings expectations, I made the case for regional diversification. This quarter is showing exactly why it matters.

What the Oil Market Is Really Saying

Most people look at the price of oil today. I prefer to look at where the market thinks oil is going.

That’s where the forward curve comes in. The forward curve shows oil prices for future delivery dates. Right now, the curve is in backwardation, which means the market expects supply to stay tight for some time.

The market is not treating this as a short-term spike. It’s pricing in tighter supply conditions for longer.

And that feeds directly into inflation.

How Oil Flows Into Inflation

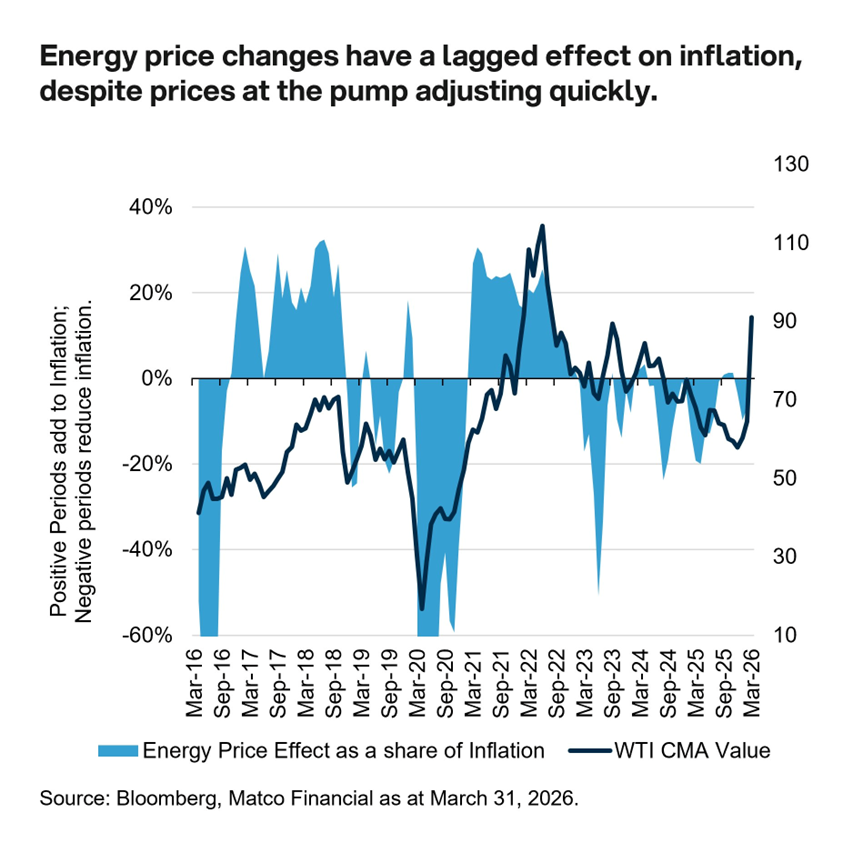

Oil is one of the biggest inputs into inflation. It affects gas prices, shipping costs, manufacturing, and everyday goods. But the impact is not instant. Think of it like a pipeline. Oil prices move first, and then over time those higher costs work their way through to consumer prices.

The chart above makes this relationship clear. Look at 2020 into 2021. When WTI crashed below $30 during the pandemic, energy’s contribution to inflation went deeply negative. It was pulling CPI down. Then as oil recovered and surged past $100 through 2021 and into 2022, the energy contribution swung sharply positive and became a major inflation driver. But notice the lag. Oil moved first. The inflation impact followed months later.

We’re seeing the early stages of a similar setup now. WTI has climbed back toward the $85-90 range, and on the right side of the chart you can see the energy contribution to inflation starting to turn positive again. The pipeline is filling up.

Said simply: oil spikes now, inflation shows up later.

Who Wins and Who Feels the Pressure

Higher oil prices don’t hit everyone at the same time or in the same way. Energy producers and commodity-linked businesses benefit immediately, which is exactly what we’re seeing in markets like Brazil and Australia this quarter. On the other side, transportation companies, consumer discretionary spending, and energy-intensive manufacturers feel the squeeze. Higher energy costs act like a tax on consumers. People spend more on fuel and less on everything else, and when that happens, demand starts to slow.

But that slowdown is where the next chapter of this story begins.

Where the Opportunity Is

Higher oil prices push inflation up at first. But over time, they slow the economy. When growth slows, central banks respond. Rates stop rising. Then they fall. That shift supports growth companies. The same businesses that often see valuation pressure during inflation spikes. In other words, the companies getting cheaper right now may be the ones that benefit most from the policy response that comes next.

Matco Positioning

Using the stoplight framework, I would call this environment yellow with a green tint. Not a full green. Inflation uncertainty and geopolitical risk deserve respect. But the fundamental picture for quality growth businesses remains strong, and the recent pullback has given us a chance to act.

Microsoft saw its shares pull back in March despite continued strength in cloud revenue and its leadership position in AI infrastructure. Cash flow generation remains among the best in the market. We added to our position during the dip because the long-term thesis hasn’t changed. The price just got more attractive.

Meta Platforms has been a similar story. The company continues to improve operating efficiency while growing earnings at a strong clip. Short-term sentiment around ad spending in a slower economy has weighed on the stock, coupled with questions about its investments in AI but the underlying business is performing well. We added to our position in during the stock price declines in March.

The Matco Global Equity Fund (Series O) pulled back 4.12% in March, in line with broader market weakness. As of March 31, Year-to-date, the fund is up 1.19%. Over the past year, we’re up 17.14%, and the three-year annualized return sits at 14.58%. Short-term volatility is the price of admission for long-term compounding.

The Bottom Line

Oil price spikes don’t just move markets in the moment. They move through the economy over time. First through energy prices, then through broader inflation, then through consumer spending, and eventually through central bank policy.

We are in the early part of that sequence now. The pipeline is filling, but we haven’t seen the full impact on CPI yet. The May and June inflation prints will be the ones to watch. That’s when the current oil environment should start showing up in the data.

Our focus remains the same: stay disciplined, stay invested, and use short-term weakness to buy high-quality businesses that can grow through the cycle. That approach has served us well, and I believe it will again.