As an investment team, the Portfolio Managers at Matco Financial come together twice a year to publish a condensed market outlook. The team identifies investment themes and revisits them as the year progresses, while also addressing new developments within their respective asset classes.

If you’re interested, here is the most recent issue.

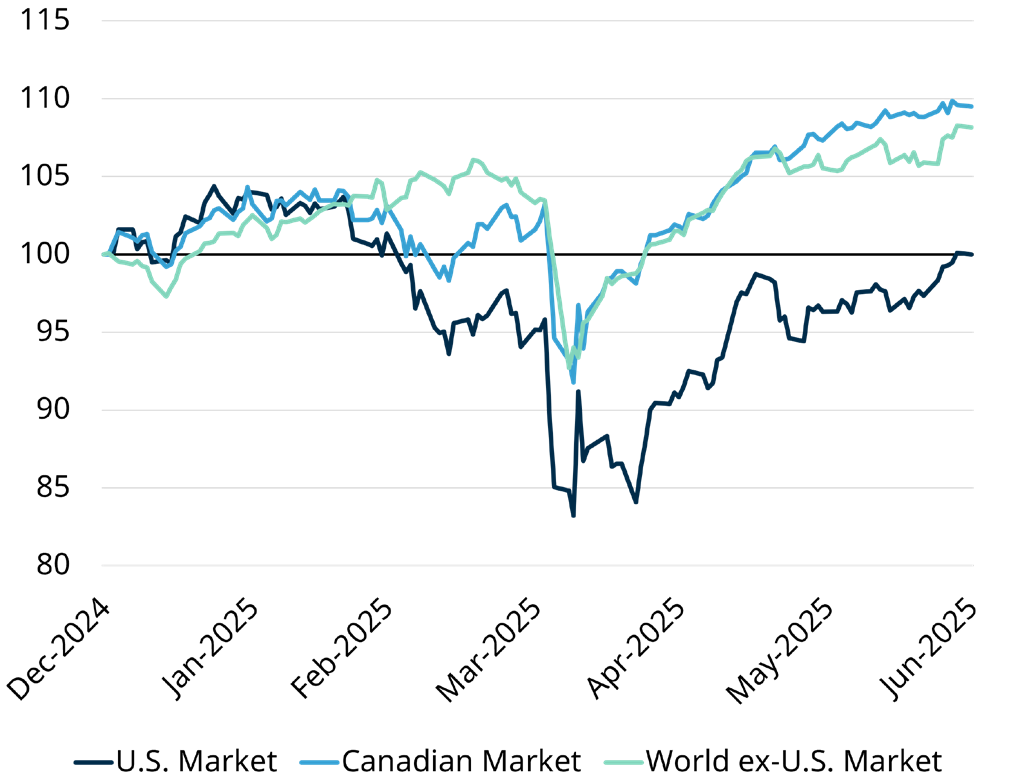

World Markets 2025

Source: FactSet Data & Analytics, Matco Financial Inc. as at June 30, 2025.

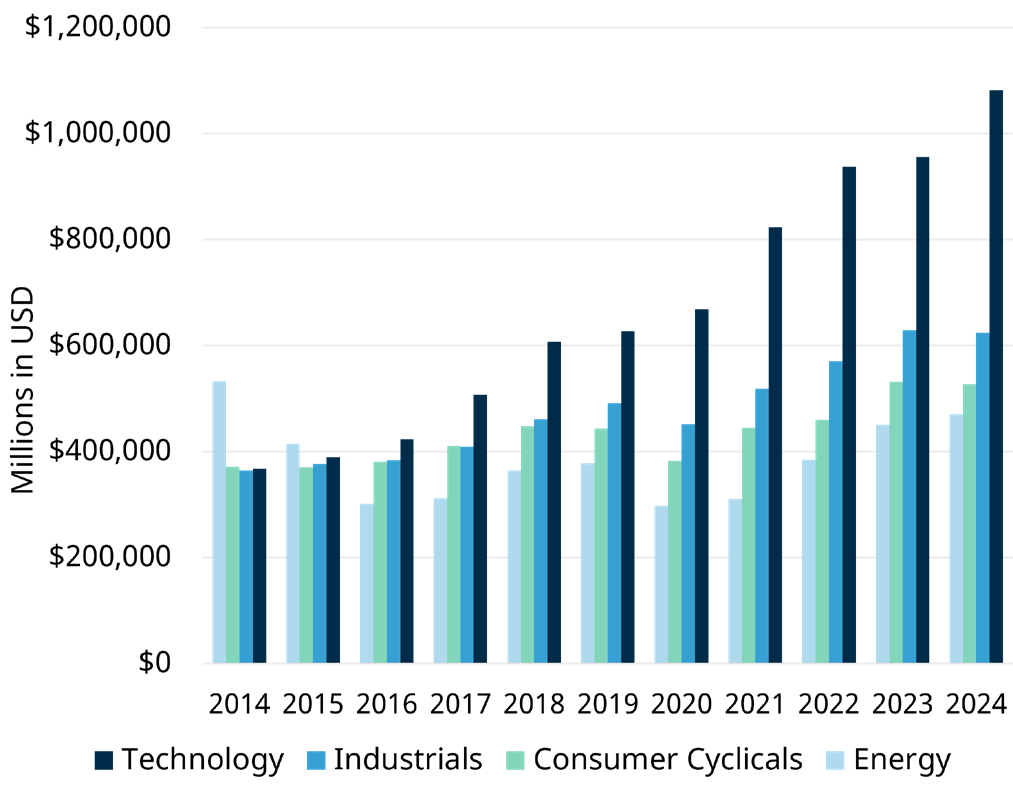

For June’s World of Opportunity edition, I wanted to expand on the Artificial Intelligence (A.I.) theme discussed in the mid-year outlook and explore the scale of business investment being made in 2025. The numbers are staggering. In 2024, publicly traded companies in the technology space spent over a trillion dollars, and they are on pace for another step up in spending this year.

Business Investment Over Time

Source: FactSet Data & Analytics, Matco Financial Inc. as at June 30, 2025.

In my view, technology investment is typically understated. Following COVID, we began to see larger capital expenditures in the sector—similar to how other industries make significant business investments. However, in technology, a massive portion of investment takes the form of research and development (R&D) expenses. R&D is mostly expensed directly on the income statement (we’ll skip the nuances of accounting frameworks—I’ve adjusted the charts accordingly). Because of this, it often goes unnoticed, which I believe is a mistake.

R&D spending tends to be overlooked due to its speculative nature—there’s no guarantee of success—and because it’s usually directed toward non-capital goods such as salaries, lab testing, and product trials, all of which are expensed rather than capitalized.

This accounting treatment is conservative, which is good from a financial reporting perspective. But when evaluating technology investments, it’s important to understand that the lead time to bring a product to market is often measured in years—and the initial R&D is a critical first step. Management teams make deliberate investment decisions to pursue the next breakthrough, and this expense should be part of an investor’s evaluation process.

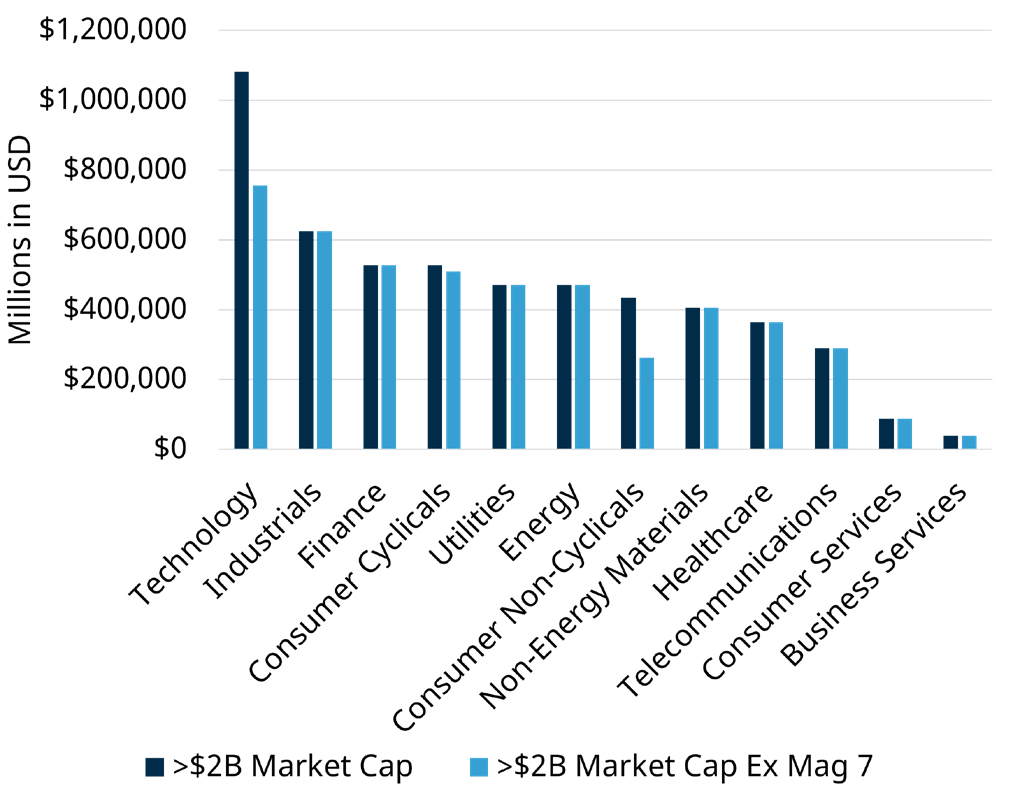

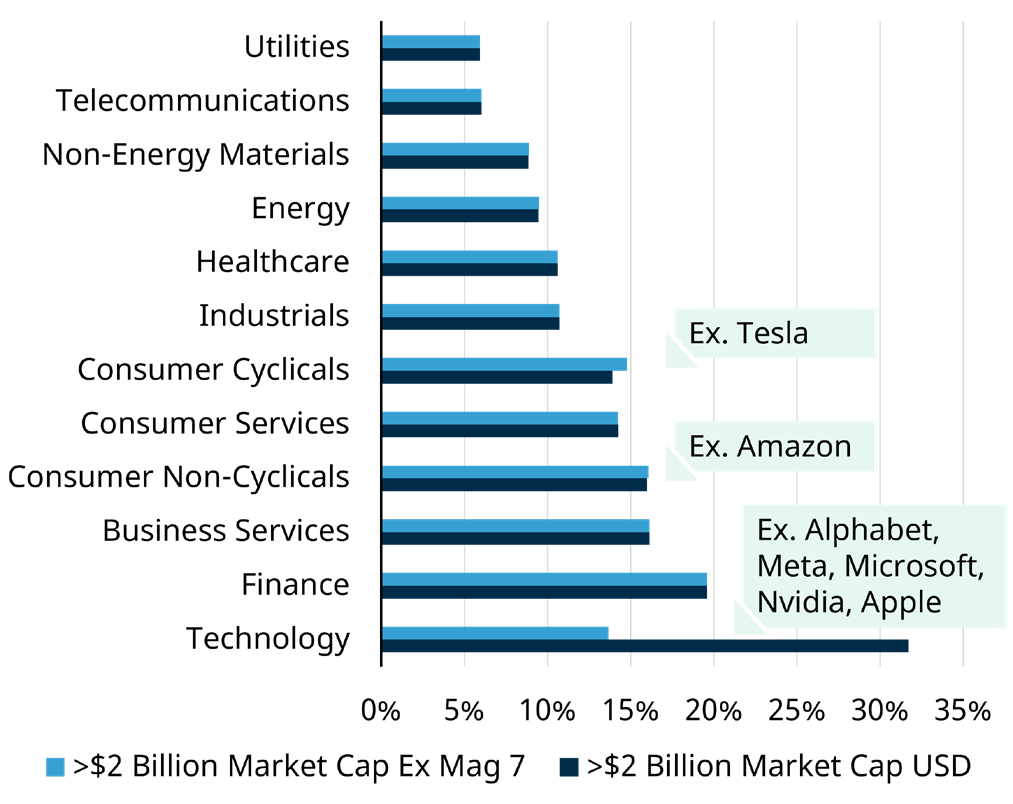

Market concentration has been a recurring topic in recent years. The impact of the so-called “Magnificent Seven” (Apple, Amazon, Alphabet, Meta, Microsoft, Nvidia, and Tesla) is clearly visible in business investment data. Not all of these companies are categorized as technology businesses—FactSet classifies Tesla as consumer cyclical and Amazon as consumer non-cyclical. However, Apple, Alphabet, Meta, Microsoft, and Nvidia collectively represent 30% of total business investment in the technology sector. Amazon accounts for 40% of the consumer non-cyclicals’ total, while Tesla contributes just 3% to consumer cyclicals.

2024 Business Investment by Sector

Source: FactSet Data & Analytics, Matco Financial Inc. as at June 30, 2025.

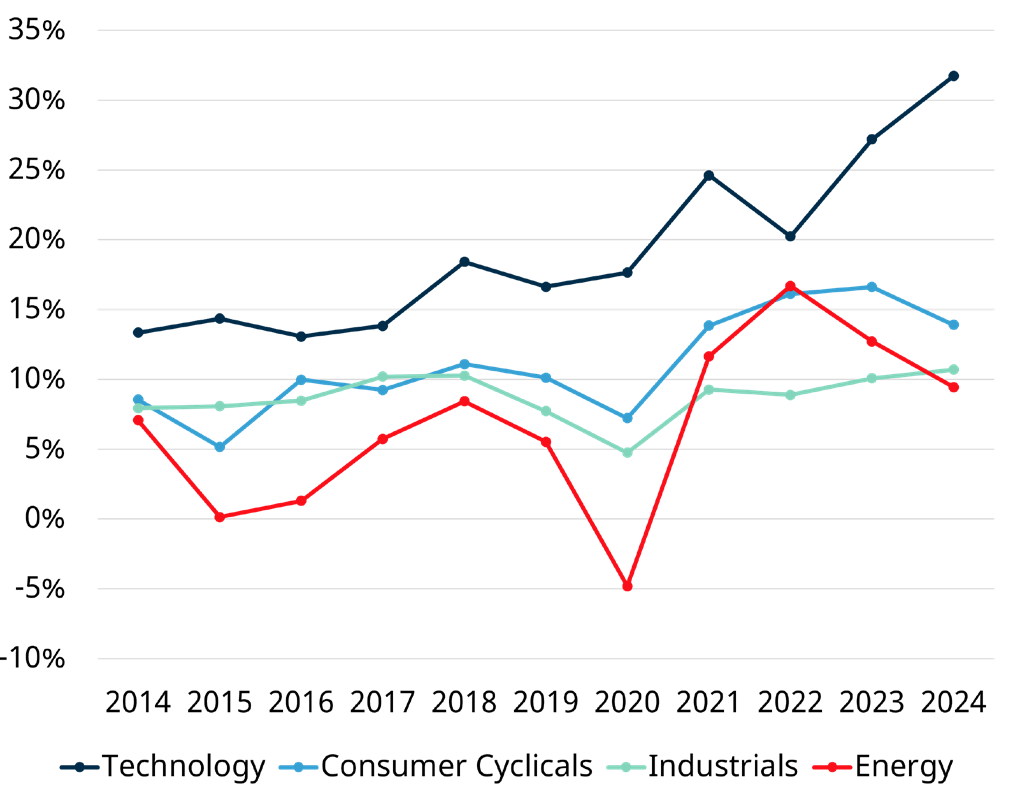

Successful business investment compounds over time and eventually shows up in a company’s earnings and cash flows. One common way to measure this is through return on invested capital (ROIC). While ROIC isn’t appropriate for every business model (e.g., banks), I’ve adjusted the chart accordingly. You’ll notice the steady rise in ROIC for the technology sector—one of the reasons we continue to see new business investment in the space. To state the obvious: it’s profitable.

Return on Invested Capital

Source: FactSet Data & Analytics, Matco Financial Inc. as at June 30, 2025.

Just as the Magnificent Seven have skewed business investment figures, they’ve also influenced ROIC numbers due to their size and profitability. Interestingly, there’s a significant step down in ROIC when Apple, Alphabet, Meta, Microsoft, and Nvidia are removed from the tech sector. The takeaway? Not all technology businesses are attractive investments. Active portfolio management can help investors avoid the worst performers.

2024 Return on Invested Capital

Source: FactSet Data & Analytics, Matco Financial Inc. as at June 30, 2025.

A large portion of the recent increase in business investment has gone into data centers, A.I. model development, software improvements, and similar areas. Reviewing management’s historical success with strategic investments provides some reassurance regarding their ability to monetize A.I. opportunities. While many uncertainties remain, some tech companies have demonstrated a consistent ability to allocate capital toward growth effectively.

From my perspective, to express a view on this investment theme, I’ve chosen to invest in businesses across different levels of the A.I. value chain. At the base are the “nuts-and-bolts” businesses—semiconductor companies and data centers building the infrastructure to power A.I. These firms are already seeing the effects of today’s spending. Next are the model developers, offering tools and A.I. platforms to public and corporate users. Finally, there are the adopters—companies integrating A.I. into their operations to unlock new revenue streams or improve efficiency.

Time will tell how profitable this technology wave will be and who the ultimate winners and losers are. In the meantime, following the money—focusing on business investment and profitability—offers the most rational path and positions us for the highest probability of success through this cycle. The real art lies in making these investments at reasonable valuations, further improving our odds.