On one side is earnings growth. Big, powerful, and hard to ignore. The first quarter reporting season has been extremely strong, and expectations for the balance of 2026 have continued to move higher.

On the other side is inflation. Also big, also powerful, and unfortunately also hard to ignore. Consumer and producer prices have reaccelerated, with the latest economic releases coming in hotter than expected.

That is the state of the investment landscape today. It is not perfect. It rarely is. But what makes this environment unique is how little “middle ground” there appears to be. One side of the ring is very positive. The other side is very negative. Investors are left watching to see which force moves the market next.

The Positive Side: Earnings Are Doing the Heavy Lifting

Let’s start with the good news.

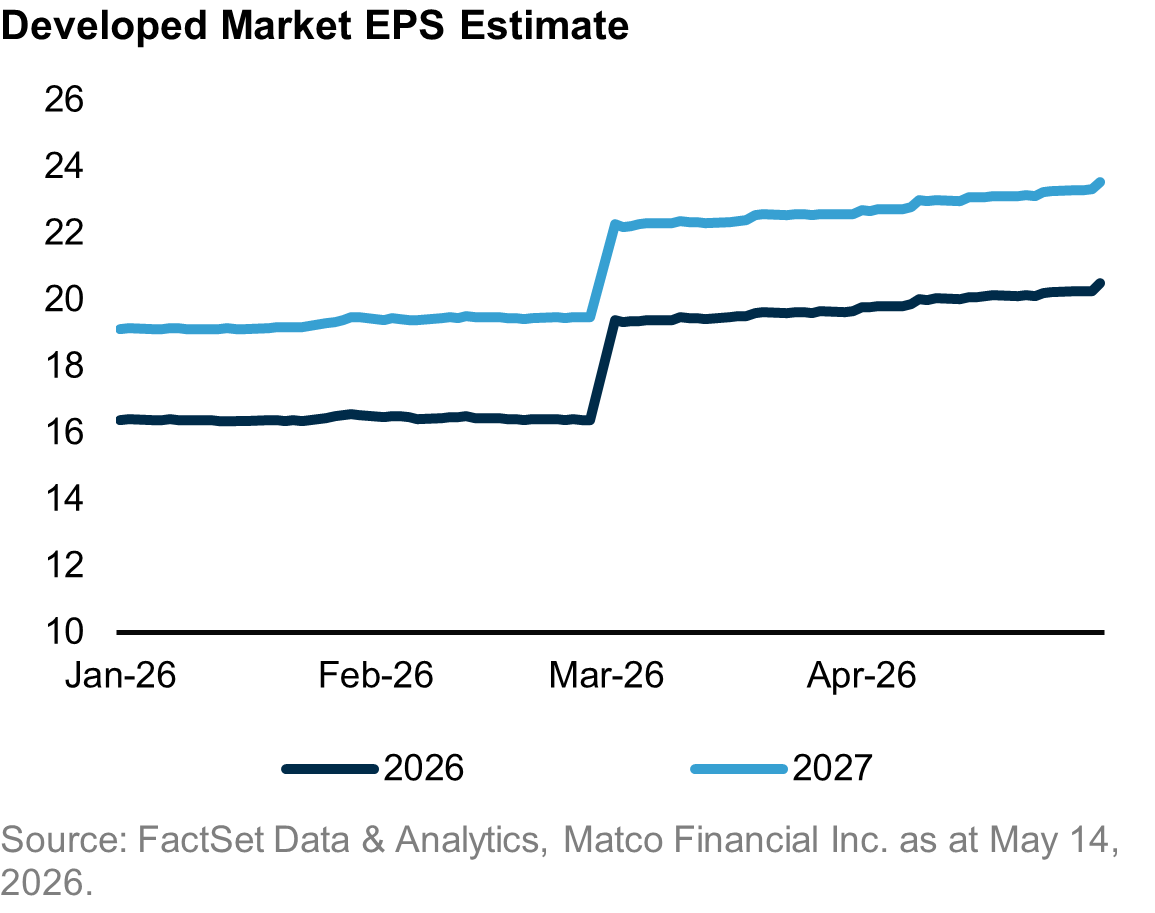

Corporate earnings have been strong, and expectations have moved higher. For the FactSet Developed Market Index, earnings per share growth for 2026 is now expected to be 25.98%, followed by another 15% in 2027. Sales growth expectations for 2026 are also healthy at 8.72%.

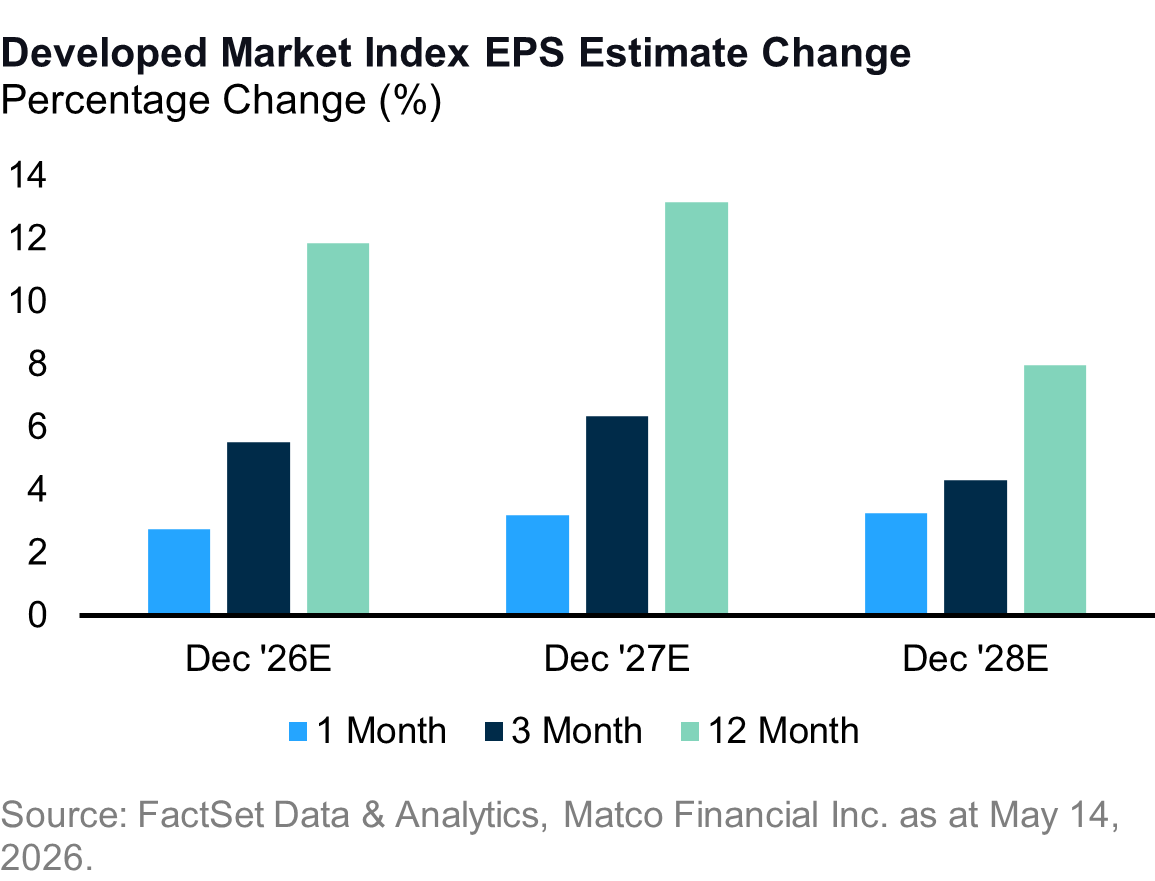

Just as important, analyst revisions have been positive. EPS estimates have increased 2.8% over the last month and 5.5% over the last three months.

That matters.

Earnings revisions are one of the cleaner ways to measure whether the fundamental backdrop is improving or deteriorating. Markets can move around for all kinds of reasons in the short term, but when analysts are revising earnings higher, it usually means companies are reporting better results, giving better guidance, or both.

Said another way, this is not just a market being pulled higher by valuation expansion. The earnings side of the equation is contributing.

As we discussed in previous newsletters, valuation needs context. A higher valuation supported by better sales, expanding margins, and improving earnings is very different from a higher valuation built only on optimism. Today, the earnings wrestler is not standing in the ring on hope alone. There is real fundamental weight behind it.

The Negative Side: Inflation Has Re-Entered the Conversation

Now for the other side of the ring.

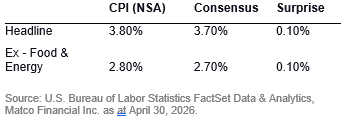

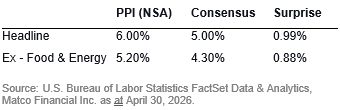

Inflation has reaccelerated. Both the Consumer Price Index and Producer Price Index came in above expectations in April.

The issue is not simply that headline inflation is higher. The real question is what degree the energy inflation we are seeing makes its way into core inflation.

Energy prices can move around quickly. They are volatile by nature. But when higher energy costs begin flowing into transportation, logistics, materials, wages, and ultimately end prices, the inflation picture becomes more complicated. That is when central banks start to pay closer attention.

This is where patience becomes difficult.

Economic data is lagged and slow. We are looking at numbers that reflect activity that has already happened, and it may take several months before we know whether this inflation pressure is temporary or more persistent. In the meantime, markets will be forced to weigh strong earnings against the possibility that central banks may need to keep policy tighter for longer.

The Central Bank Question

This brings us to the referee in the ring: central banks.

The key question is whether the latest inflation data leads to another hiking cycle or a period of patience.

A hiking cycle would mean central banks increase target rates to slow demand and bring inflation back under control. That would likely put pressure on valuations, particularly for longer-duration growth assets where a larger portion of value is tied to future cash flows.

A patience approach would mean holding rates at current levels and waiting for clarity on whether this is an energy-driven supply shock or something more embedded in the economy.

There is a big difference between those two paths.

If inflation is largely tied to an energy supply shock, raising rates may not solve the immediate problem. Higher interest rates do not produce more oil or reopen supply routes. However, if higher energy costs begin feeding into broader inflation expectations and wage demands, central banks may decide they need to act.

This is the messy middle we have talked about before. Not bad enough to abandon equities, not clean enough to ignore risk.

Using the stoplight analogy, I would not call this a red light. Earnings are too strong for that. But I would also hesitate to call it a full green light. Inflation has moved the light back toward yellow.

Why Quality Matters Here

In my view, this is exactly the type of environment where quality matters.

To manage the inflation and interest rate risks, while still participating in the current earnings cycle, we continue to focus on quality companies.

Why?

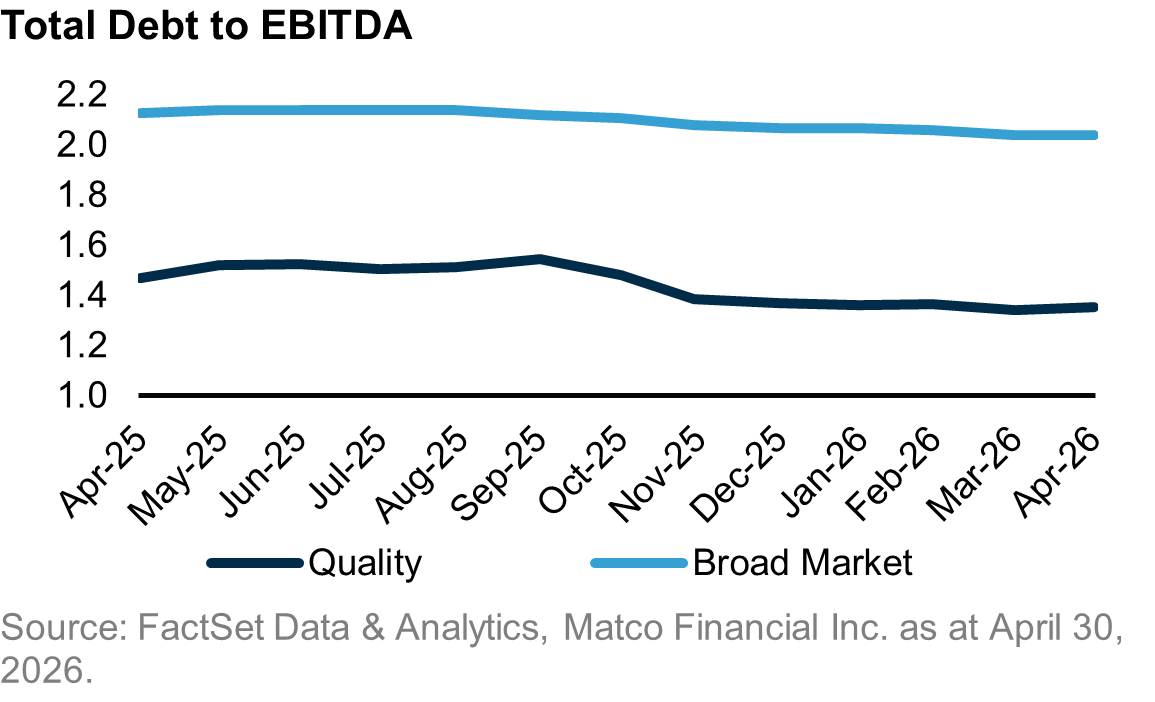

First, quality companies typically have lower debt levels. That matters when interest rates are higher, because less debt means less sensitivity to rising interest expense. A company with a stretched balance sheet can see earnings pressure quickly when borrowing costs move higher. A company with a strong balance sheet has more flexibility.

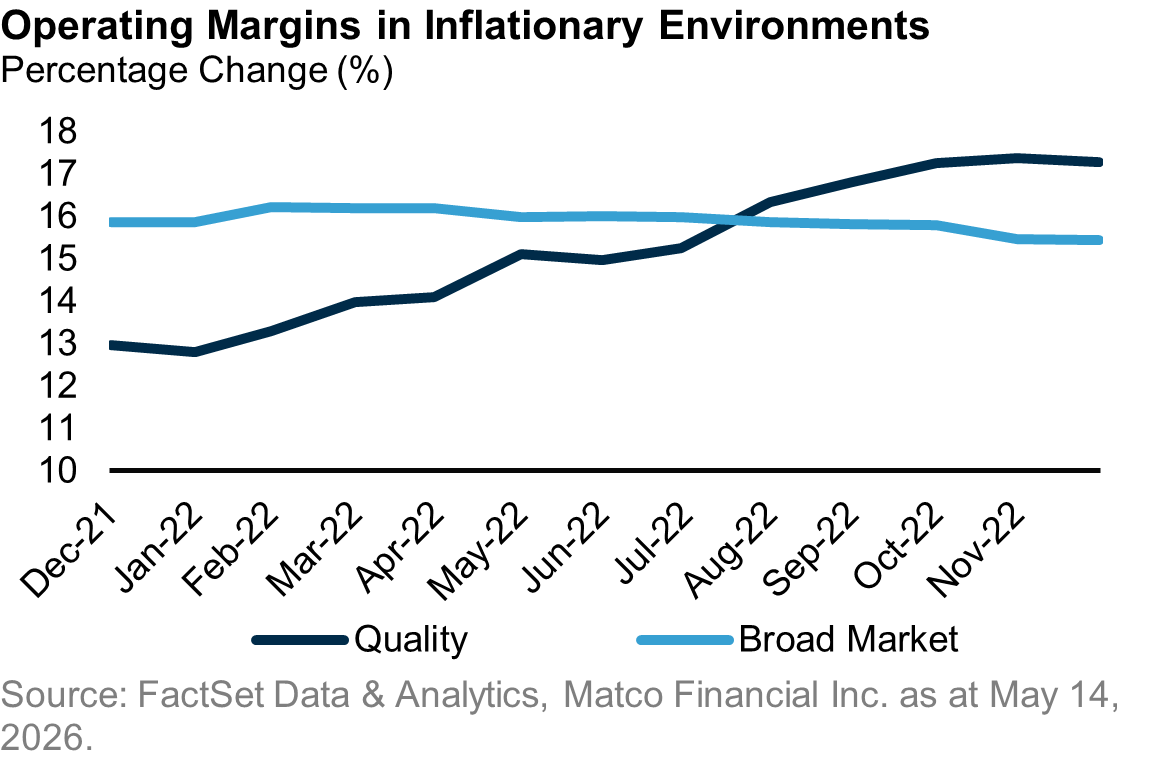

Second, quality companies often have pricing power. In an inflationary environment, the ability to defend margins is critical. Not every business can pass through higher costs. Some companies are price takers. Others have products, services, brands, or market positions that allow them to protect profitability.

Third, quality companies are compounders. They reinvest capital, grow earnings, generate cash flow, and reward shareholders over time. This strategy will not win a lot of attention at a cocktail party. It is not built for the loudest headline of the week. But it has been proven through market cycles to build wealth.

This is the same framework we have discussed in prior issues: wide moat businesses, growing cash flows, and management teams with strong execution records. The environment changes, but the building blocks remain the same.

Matco Global Equity Fund positioning

Within the Matco Global Equity Fund, we continue to balance participation in the earnings cycle with risk management around inflation and interest rates.

That means staying invested, but being selective. It means looking for companies that can grow through a range of economic conditions, rather than only in perfect conditions.

Fortinet — a cybersecurity company that blends networking and security, selling a broad platform of firewalls, SASE, security operations, and related tools to over half a million customers.

Cheniere Energy — a leading U.S. LNG exporter that owns and operates major liquefaction/export terminals on the Gulf of Mexico.

MasterCard — a global payments technology network that enables secure digital transactions across 200+ countries and territories.

The point is not to predict exactly which sumo wrestler wins the next round. The point is to build a portfolio that can handle the match.

If earnings continue to improve and inflation settles down, quality companies should participate. If inflation remains sticky and rates stay higher for longer, quality companies should be better positioned to defend margins and manage financing costs.

The Bottom Line

The investment ring is crowded today.

On one side, corporate earnings are strong and expectations are rising. On the other side, inflation has reaccelerated and central banks may need to stay cautious.

That tension is uncomfortable, but it is not unusual. Markets rarely offer perfect conditions. More often, investors are asked to make decisions with one eye on opportunity and the other on risk.

For us, the answer remains consistent: stay invested, stay diversified, and focus on quality businesses that can compound earnings and cash flows through different market environments.

The sumo match may take time to play out. Our job is not to guess every move. Our job is to own the businesses that can stay standing.